Who’s Responsible for Insurance During the Settlement Period in Australia?

Manish Bansal | 2026/02/27

Manish Bansal | 2026/02/27

Who’s Responsible for Insurance During the Settlement Period in Australia?

Buying or selling a property is exciting but between exchange and settlement, there’s a period where many people assume everything is “sorted.”

Legally, it’s not that simple. One of the most overlooked (and potentially costly) questions in a property transaction is, "Who is responsible for insuring the property during the settlement period?"

The answer depends entirely on which state or territory the property is in and the rules vary more than most people realise.

What Is the Settlement Period?

The settlement period is the time between:

- Exchange of contracts – when the agreement becomes legally binding, and

- Settlement day – when ownership officially transfers and funds are paid.

This period typically lasts 30 to 90 days. During this time, the property still legally belongs to the seller but in some states, the risk of damage may already have transferred to the buyer. And that’s where insurance becomes critical.

What Does “Risk” Actually Mean?

“Risk” refers to who bears the financial responsibility if the property is damaged before settlement.

For example:

- Fire

- Storm damage

- Flooding

- Vandalism

- Structural issues caused by unforeseen events

If something happens before settlement, the question becomes, Who is legally responsible, the seller or the buyer?

The answer depends on the state.

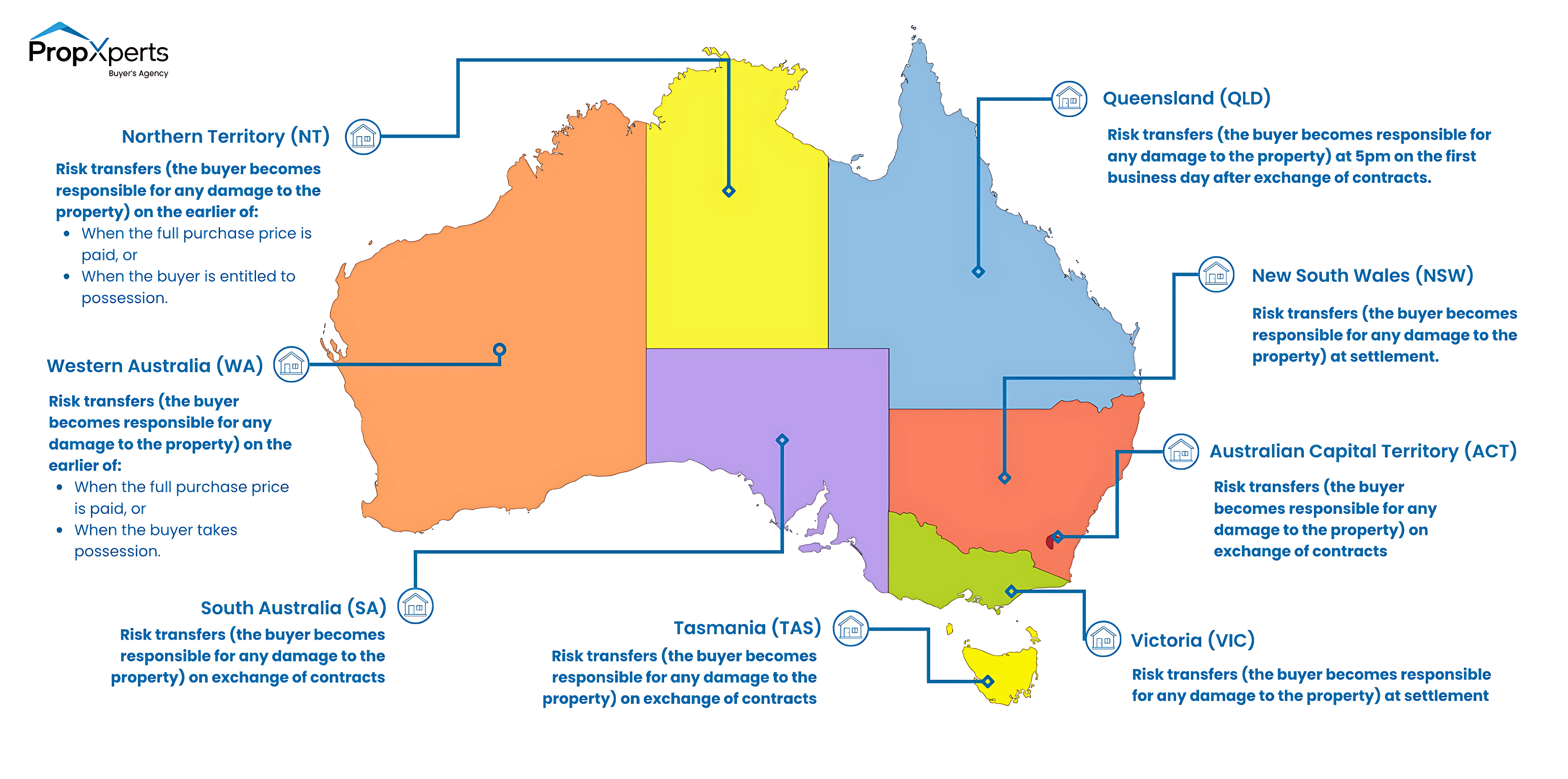

Insurance Responsibility by State and Territory

Here’s how it works across Australia:

- New South Wales (NSW) : Risk transfers (the buyer becomes responsible for any damage to the property) at settlement

The seller remains responsible for the property up until settlement day. However, many buyers still arrange insurance from exchange as a precaution.

- Victoria (VIC) : Risk transfers (the buyer becomes responsible for any damage to the property) at settlement

Similar to NSW, the seller carries the risk until settlement. Buyers should still check their lender’s insurance requirements.

- Queensland (QLD) : Risk transfers (the buyer becomes responsible for any damage to the property) at 5pm on the first business day after exchange of contracts

This catches many buyers off guard. In Queensland, the buyer can become responsible almost immediately after contracts are signed.

Best practice: Arrange insurance as soon as contracts are exchanged.

- South Australia (SA) : Risk transfers (the buyer becomes responsible for any damage to the property) on exchange of contracts

Once contracts are signed, the buyer bears the risk. Insurance should be active from exchange.

- Tasmania (TAS) : Risk transfers (the buyer becomes responsible for any damage to the property) on exchange of contracts

Buyers should ensure insurance is in place from the moment contracts become binding.

- Australian Capital Territory (ACT) : Risk transfers (the buyer becomes responsible for any damage to the property) on exchange of contracts

The buyer assumes responsibility from exchange.

- Western Australia (WA) : Risk transfers (the buyer becomes responsible for any damage to the property) on the earlier of

- When the full purchase price is paid, or

- When the buyer takes possession.

This often aligns with settlement, but buyers should confirm details in their contract.

- Northern Territory (NT) : Risk transfers (the buyer becomes responsible for any damage to the property) on the earlier of

- When the full purchase price is paid, or

- When the buyer is entitled to possession.

Similar framework to WA.

Note: This image is a simplified visual guide created for easier understanding.

Why This Matters?

Consider this scenario:

You exchange contracts, the settlement is 60 days away, a severe storm damages the roof.

In:

- NSW or VIC → The seller’s insurance typically covers it.

- QLD, SA, TAS, ACT → The buyer is responsible.

And importantly, the buyer may still be legally required to proceed with settlement — even if the property has been damaged. Without appropriate insurance, that could create significant financial stress.

Practical Advice for Buyers

Regardless of your state, it’s generally wise to:

- Arrange building insurance from exchange (or earlier if required)

- Confirm lender insurance conditions

- Ensure coverage reflects full replacement value

- Check strata insurance if purchasing a unit or apartment

Even in states where risk transfers at settlement, taking out insurance early provides added protection and peace of mind.

A Note for Sellers

Sellers should maintain insurance until settlement has been completed and ownership has officially transferred. Cancelling insurance early can expose you to unnecessary risk if damage occurs before settlement.

Quick Reference Summary

Final Thoughts

There is no single national rule governing insurance responsibility during the settlement period in Australia. Each state and territory has its own position and misunderstanding the timing of risk transfer can have serious financial consequences. Before exchanging contracts, speak with your solicitor or conveyancer to confirm your obligations and ensure insurance is arranged at the appropriate time. When it comes to property, clarity and preparation make all the difference.

Disclaimer : The information provided in this blog is general in nature and is intended for educational purposes only. It does not constitute legal, financial, or insurance advice. Laws, contract terms, and insurance requirements may vary depending on your state or territory, lender conditions, and individual circumstances. Readers should consult their solicitor, conveyancer, and directly confirm details with their insurer to verify coverage, policy start dates, and specific obligations before making any decisions.

Thank You

Your message has been sent successfully. We'll get back to you soon!